A budget is one of the simplest tools for reaching financial goals. At its core, a budget helps you plan how to use your money so you can cover essential bills, build savings and still enjoy life. Yet many people abandon their budgets because the plan was unrealistic or too strict. When a budget doesn’t account for irregular expenses, includes every penny without room for fun or ignores the emotional side of money, it’s hard to follow. A successful budget balances discipline with flexibility and works with your lifestyle rather than against it.

This guide explains how to create a budget you can actually stick to. It uses credible sources like the Consumer Financial Protection Bureau (CFPB), USA.GOV, NerdWallet and MMBB to illustrate best practice budgeting methods. Whether you’re paid monthly, freelance or juggling multiple priorities, these steps will help you build a realistic system that survives everyday challenges.

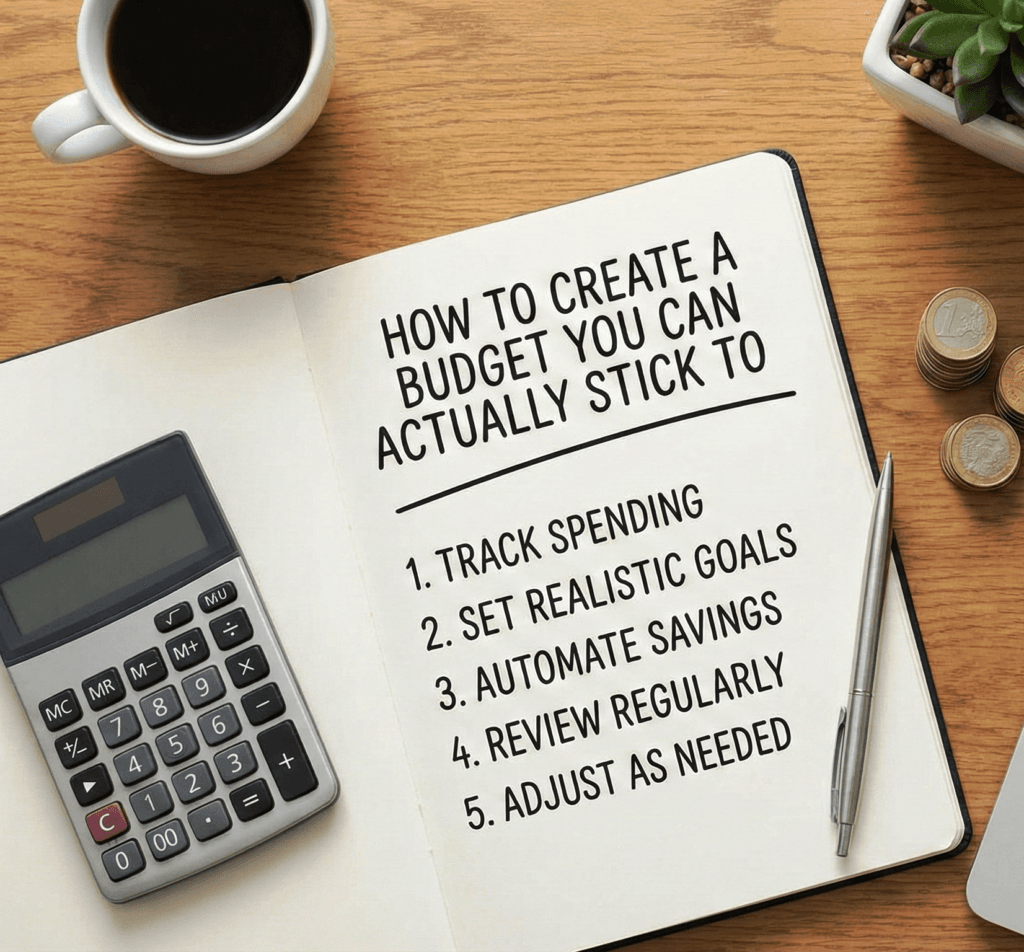

1. Clarify why you’re budgeting

Before you decide how to allocate your income, think about why you want a budget. A vague goal like “save more” rarely motivates behavior change. Clear, specific objectives help you stay committed when temptations arise. Examples include:

- Build an emergency fund large enough to cover three months of expenses.

- Pay off a specific debt, such as a credit card balance, within a defined time frame.

- Save for a long‑term purchase, like a laptop, wedding or down payment on a home.

- Reduce money stress, so you don’t feel anxious about bills or unexpected expenses.

By connecting your budget to meaningful goals, you create a purpose for each spending choice. This “why” also guides trade‑offs later: if dining out cuts into your emergency fund savings, you’ll know which is more important.

2. Determine your net income and baseline expenses

We need to determine your net income and expensive through these following parameters.

2.1. Collect your after tax income

Budgeting starts with knowing how much money you actually bring home. Your net income is what’s left after taxes, insurance premiums, retirement contributions and other deductions. Gather pay stubs, freelance invoices, benefits statements or other income records to get a complete picture. The CFPB recommends recording all sources of income including multiple jobs, self‑employment and government benefits so you know what you have available each month.

2.2. Track where your money goes

Next, track your spending over at least two or three months. Don’t rely on memory or guesswork use your bank statements, credit card bills and receipts to categorize purchases. The CFPB’s Spending Tracker helps you log expenses by category (utilities, groceries, entertainment, etc.). If the process feels overwhelming, start small: review one week at a time or keep a daily log for a month to capture small purchases like coffee or snacks.

This detailed tracking gives you a real baseline rather than an idealized version of your spending. You may discover that routine subscriptions or impulse purchases add up. For each expense, note whether it’s a need, want or saving/debt payment.

2.3. Separate needs, wants and savings

One popular framework for categorizing expenses is the 50/30/20 budget. NerdWallet explains that this plan allocates 50% of after tax income to necessities, 30% to wants and 20% to savings and debt repayment. According to the article:

- Needs (up to 50%) include groceries, housing, basic utilities, transportation, insurance, minimum debt payments and child care. If basic needs exceed 50%, you can temporarily draw from the “wants” category, but persistent overages suggest your budget needs adjusting.

- Wants (around 30%) cover discretionary spending like dining out, gifts, travel and entertainment. NerdWallet emphasizes that budgets shouldn’t be too strict; allowing some fun money makes them easier to stick with.

- Savings and debt repayment (20%) fund your future and help you pay down balances faster. Examples include building an emergency fund, saving for retirement or making extra loan payments.

If 50/30/20 doesn’t align with your situation, adjust the percentages. NerdWallet suggests that people may need a 60/20/20 split (60% needs, 20% wants, 20% savings) or another ratio depending on income, family size and cost of living. The point is to ensure that each paycheck covers essentials, allows some personal enjoyment and prioritizes saving.

3. Choose a budgeting method that suits you

There’s no single “best” way to budget. The most effective method is the one you’ll actually maintain. Below are three popular approaches, along with their pros and cons.

3.1. Budgeting rule 50/30/20

The 50/30/20 rule, described above, is praised for its simplicity. The MMBB article explains that the rule divides after‑tax income into three broad categories (needs, wants and savings). Its strengths include:

- Easy to understand: Because there are only three buckets, beginners can quickly adopt it.

- Flexibility: You have discretion within each category to prioritize spending and adjust from month to month.

- Balanced approach: By allocating money to needs, wants and savings, you avoid ignoring any part of your financial life.

However, the rule may not work for everyone. The broad categories can oversimplify spending, and the percentages may not align with your cost of living. If your income is low or your housing costs are high, your needs may exceed 50%. If so, adjust the ratios or switch methods.

3.2. Zero based budgeting

Zero based budgeting (ZBB) is more granular. The MMBB article defines ZBB as assigning every dollar a purpose so that income minus expenses equals zero. Each expense, from groceries to entertainment, is planned ahead of time. Pros include detailed tracking, financial control and adaptability. You can tailor the budget to specific goals like debt payoff or saving for a major purchase.

On the downside, ZBB can be time consuming and overwhelming for beginners. It may feel rigid if unexpected expenses pop up. If you’re new to budgeting, you might combine ZBB for some categories (e.g., groceries, utilities) with a broader 50/30/20 approach for discretionary spending.

3.3. Pay yourself first (reverse budgeting)

The pay yourself first method flips traditional budgeting: you prioritize savings before deciding how much to spend on other categories. A SmartAsset guide explains that automatic savings involves instructing your bank to transfer a predetermined amount from your checking to a separate savings or investment account at regular intervals. By automating transfers say, $100 every two weeks your savings grow consistently without requiring willpower. Benefits of automatic savings include:

- Consistency: Regular transfers establish a disciplined saving habit.

- Ease: Once set up, you don’t have to remember to move money manually.

- Goal achievement: Automatic transfers help you reach goals like an emergency fund, vacation or down payment.

- Financial security: A savings cushion provides a safety net for unexpected expenses.

- Investment opportunities: Regular savings can be moved into stocks, bonds or retirement accounts when the balance is large enough.

- Reduced impulse spending: Funds moved to savings are less available for day to day spending, which can curb unnecessary purchases.

Reverse budgeting works well for people who struggle to save consistently. You decide on a savings amount first, automate it, and then live on the remainder. If you have irregular income, set your baseline savings percentage based on your lowest average monthly earnings and increase contributions in high income months.

4. Account for real life expenses

A budget that ignores irregular or unexpected costs is a recipe for failure. To make a budget stick, include the messy parts of real life.

4.1. Build a “life buffer” and plan for irregular costs

Even a modest life buffer (a separate category for small surprises) can prevent a single unexpected expense from derailing your budget. Budget for occasional expenses such as car repairs, medical visits, school supplies, gifts and annual fees. The usa.gov article notes that planning for unexpected expenses is essential and suggests using tools from the Department of Labor to develop a savings plan and build an emergency fund. Divide annual or quarterly expenses by 12 and save that amount each month.

For example, if you pay USD 2400 per year in car insurance, set aside USD 200 each month. Similarly, if you expect to spend USD 3000 on holiday gifts, save USD 250 each month starting in January. Spreading irregular costs over the year smooth cash flow and prevent panic when the bill arrives.

4.2. Track due dates and avoid late fees

According to the CFPB, missing payments or paying late can have larger impacts on your credit scores and overall financial well-being. Use a bill calendar or digital reminders to record when bills are due. Align automatic payments with your pay cycle to ensure funds are available. Many budgeting apps send notifications before bills are due; use whichever tools are easiest for you.

4.3. Allow room for joy

Budgets shouldn’t feel like punishment. NerdWallet stresses that even when you’re trying to get out of debt fast, including some fun money makes it easier to stick with the plan. Denying yourself all pleasures often leads to burnout and excessive spending. Decide how much you can reasonably allocate to dinners out, streaming subscriptions or hobbies. If money is tight, look for low‑cost or free ways to enjoy life, like cooking with friends or exploring local parks.

5. Automate savings and bill payments

Automation is a powerful way to stick to a budget because it removes the need for constant willpower. The SmartAsset article highlights several steps to create an automatic savings strategy:

- Identify your financial goals: Define what you’re saving for (emergency fund, down payment, retirement) and how much you need.

- Determine how long you’ll save: Decide whether your plan is short term (e.g., six months for a vacation) or long term (ongoing retirement contributions).

- Create a budget: Evaluate monthly income and expenses to determine how much you can realistically save. This ensures your automatic deposits won’t leave you unable to pay essentials.

- Choose a savings vehicle: Pick a high‑yield savings account, money market account, CD or investment account based on your goals. If your employer offers a retirement plan with matching contributions, automate contributions to maximize the match.

- Set up a transfer schedule: Coordinate automatic transfers with your paydays. This ensures your savings deposit occurs before the money hits your checking account and you’re tempted to spend it.

- Review monthly and adjust: Revisit your budget and savings strategy regularly. Income, expenses and goals change, so adjust transfer amounts or frequency as needed.

Automation should also include bill payments. Most utilities, phone providers and credit card issuers let you schedule automatic payments. This helps avoid late fees and ensures your budget stays on track.

6. Use simple spending rules

A budget doesn’t require tracking every purchase forever. Once you understand your spending patterns, implement a few behavior guardrails to prevent impulse buying. Examples include:

- 24 hour rule: Wait one day before purchasing non‑essential items. The cooling‑off period reduces impulse buys.

- Weekly cash limit: Withdraw a set amount of cash for discretionary spending; when the cash is gone, stop spending.

- One‑in, one‑out rule: If you buy a new item (e.g., clothing), sell or donate an old one. This ensures you’re mindful of consumption.

The usa.gov article emphasizes that monitoring spending habits and reviewing your budget regularly helps you identify areas to cut back. These simple rules add friction to spending decisions without requiring constant record‑keeping.

7. Review and adjust regularly

Budgets aren’t static. Job changes, new expenses, family additions or economic shifts can alter your financial reality. The usa.gov guide advises reviewing your budget periodically and adjusting as necessary. The CFPB also notes that updating your budget when your income or spending habits change ensures it remains realistic.

7.1. Weekly check‑ins

Spend a few minutes each week reviewing transactions and checking how much remains in each category. Ask yourself:

- Are you on track to stay within your “needs,” “wants” and “savings” allocations?

- Did any unexpected expenses occur? If so, adjust your buffer or reduce discretionary spending next week.

- Are there any recurring charges (subscriptions, memberships) you no longer use?

7.2. Monthly reset

At the end of each month, reconcile your actual spending with your planned budget. Adjust category amounts based on real life for example, if groceries always exceed the initial estimate, increase that category and reduce another. Use this time to plan for upcoming irregular expenses like annual car insurance or holiday spending.

8. Get support and use the right tools

To use the right tools for checking and supporting your budget. Following are:

8.1. Tools and trackers

Budgeting doesn’t require fancy apps, but the right tool can make it easier. The CFPB provides free worksheets, including an Income Tracker and Budget Worksheet, to help you log income, expenses and bill due dates. The Bill Calendar helps you schedule payments and see when money enters and leaves your account.

Budgeting apps like YNAB (You Need a Budget), Mint, Monarch and Tiller (mentioned by MMBB) can automate transaction import and category tracking. Some apps are subscription‑based; weigh the cost against the convenience they offer.

You can also use a simple spreadsheet, a notebook or the envelope system (cash stuffing) if you prefer tactile methods. The key is to choose a tool you’ll use consistently.

8.2. Build a support system

Sticking to a budget is easier when you have encouragement. The CFPB suggests developing a support system of family or friends who can help you stay accountable. Consider budgeting alongside a partner or joining online communities where people share progress and challenges.

If debt feels overwhelming, don’t hesitate to seek professional advice. usa.gov recommends turning to trusted experts or counseling services for help when needed. Nonprofit credit counseling agencies can review your budget, negotiate with creditors and suggest debt‑management plans.

9. Tips for staying motivated

Creating a budget is one thing; maintaining it for months and years requires mindset shifts. Here are strategies to stay motivated:

- Start small: If saving 20% feels impossible, start with 5% and gradually increase. Consistency matters more than intensity early on.

- Make progress visible: Use charts or graphs to see your debt shrinking or savings growing. Visual cues reinforce positive behavior.

- Celebrate milestones: When you hit a savings goal or pay off a loan, reward yourself in a modest way. Small celebrations keep you energized.

- Frame it as a choice, not deprivation: Instead of “I can’t buy new clothes,” think “I’m choosing to prioritize my emergency fund.” Language influences behavior.

- Allow for flexibility: Life changes. Don’t see budget adjustments as failure; view them as refinements to reflect new realities.

Conclusion

A budget you can stick to isn’t about micromanaging every purchase or denying yourself all pleasures. It’s a plan that clarifies your priorities, ensures you cover necessities, promotes saving, and leaves space for joy. Whether you use the 50/30/20 rule, zero based budgeting or a pay yourself first approach, the goal is the same: make deliberate decisions about how you use your money.

By following the steps in this guide tracking income and expenses, choosing a suitable method, planning for irregular costs, automating savings, reviewing regularly and seeking support you’ll build a sustainable budget. Over time, this habit can reduce financial stress, increase savings and help you achieve the goals that matter most to you.

Financial Disclaimer

The information provided on this blog is for educational and informational purposes only and should not be considered financial, investment, tax, or legal advice. All content is general in nature and may not apply to your individual circumstances.

While we strive to keep the information accurate and up to date, we make no warranties or guarantees regarding completeness, reliability, or accuracy. Any actions you take based on the information on this blog are strictly at your own risk.

Before making any financial decisions, you should consult a qualified professional who can consider your specific goals, income, risks, and personal situation.

Frequently Asked Questions

What is the best budgeting method for beginners?

The 50/30/20 rule is a simple way to start because it gives structure without heavy tracking. You can adjust the percentages based on your situation.

What is zero based budgeting?

Zero based budgeting assigns every unit of income a purpose so that income minus allocations equals zero. It helps prevent unplanned spending and improves clarity.

How do I stick to a budget long term?

Automate savings and bills, add a realistic buffer, and review your plan regularly. Consistent check-ins help you adapt when life changes.

Is it okay if my needs take more than 50% of my income?

Yes. The 50/30/20 rule is a guideline, not a fixed rule. In higher cost of living situations, you may need to adjust the percentages and focus on gradual improvements.

What is a budget in simple terms?

A budget is a plan for how you’ll use your money each month. It helps you cover essentials, save for goals, and avoid unnecessary debt.

What is zero based budgeting?

It’s a method where you assign every unit of income a job (needs, wants, savings, or debt) so your income minus allocations equals zero. This creates strong control and clarity.

What is the “pay yourself first” method?

You save automatically right after you get paid, then budget the rest. This reduces willpower reliance and improves consistency.